目錄

- 相關鏈接

- 1 題目

- 2 思路決議

- 3 Python 實作

- 3.1 資料分析和預處理

- 3.2 預測

- 3.3 進階的預測方案和代碼

- 3.4 動態規劃

- 3.4.1 思路方案

- 3.4.2 思路2

- 3.4.3 思路3

- 3.3.2 Python實作

更新時間:2022-2-21 15:00

相關鏈接

完整代碼和參考文獻下載

https://mianbaoduo.com/o/bread/YpeclJhr

1 題目

要求開發一個模型, 這個模型只使用到目前為止的過去的每日價格流來確定,每天應該買入、 持有還是賣出他們投資組合中的資產,

2016 年 9 月 11 日, 將從 1000 美元開始, 將使用五年交易期, 從 2016 年 9 月 11 日到2021 年 9 月 10 日, 在每個交易日, 交易者的投資組合將包括現金、 黃金和位元幣[C, G, B],分別是美元、 金衡盎司和位元幣, 初始狀態為[1000,0,0], 每筆交易(購買或銷售)的傭金是交易金額的α%, 假設

α

g

o

l

d

\alpha _{gold}

αgold?= 1%,

α

b

i

t

c

o

i

n

\alpha_{bitcoin}

αbitcoin? = 2%, 持有資產沒有成本,

請注意, 位元幣可以每天交易, 但黃金只在市場開放的日子交易(即周末不交易), 這反映在定價資料檔案LBMA-GOLD.csv 和 BCHAIN-MKPRU.csv 中, 你的模型應該考慮到這個交易計劃, 但在建模程序中你只能使用其中之一,

-

開發一個模型, 僅根據當天的價格資料給出最佳的每日交易策略, 使用你的模型和策略,

在 2021 年 9 月 10 日最初的 1000 美元投資價值多少? -

提供證據證明你的模型提供了最佳策略,

-

確定該策略對交易成本的敏感度, 交易成本如何影響戰略和結果?

-

將你的策略、 模型和結果以一份不超過兩頁的備忘錄的形式傳達給交易者,

注意: 您的 PDF 總頁數不超過 25 頁, 解決方案應包括: -

一頁摘要表, 目錄, 完整的解決方案, 一到兩頁附錄, 參考文獻,

注:MCM 競賽有 25 頁的限制, 您提交的所有方面都計入 25 頁的限制(摘要頁、 目錄、 參考文獻和任何附錄), 必須在你的報告中標注你的想法、 影像和其他材料的來源參考

2 思路決議

3 Python 實作

3.1 資料分析和預處理

(1)資料分析

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

gold = pd.read_csv('./data/LBMA-GOLD.csv')

bitcoin = pd.read_csv('./data/BCHAIN-MKPRU.csv')

gold.info()

<class ‘pandas.core.frame.DataFrame’>

RangeIndex: 1265 entries, 0 to 1264 Data columns (total 2 columns):

Column Non-Null Count Dtype — ------ -------------- -----

0 Date 1265 non-null object

1 USD (PM) 1255 non-null float64

dtypes: float64(1), object(1)

# 缺失值查看

gold.isnull().any()

Date False

USD (PM) True

dtype: bool

黃金序列存在缺失值

bitcoin.isnull().any()

Date False

Value False

dtype: bool

位元幣序列沒有缺失值

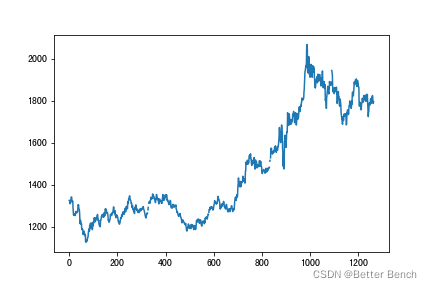

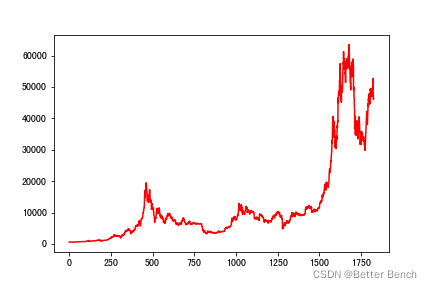

可視化資料

x1 = range(len(gold))

y1 = gold['USD (PM)']

x2 = range(len(bitcoin))

y2 = bitcoin['Value']

plt.plot(x1,y1)

plt.plot(x2,y2,color='r')

(2)資料預處理

黃金序列是有缺失值,且周末不存在資料,時間序列是中斷的,以下采用插值法進行填充資料,將補充為完整的時間序列

gold.index = list(pd.DatetimeIndex(gold.Date))

gold_datalist = pd.date_range(start='2016-09-12',end='2021-09-10')

ts = pd.Series(len(gold_datalist)*[np.nan],index=gold_datalist)

gold_s = gold['USD (PM)']

for i in gold.index:

ts[i] = gold_s[i]

# 線性插值法

ts = ts.interpolate(method='linear')

gold_df = ts.astype(float).to_frame()

gold_df.rename(columns={0:'USD'},inplace=True)

gold_df.sort_index()

gold_df.index = range(len(gold_df))

gold_df

補充完整后,黃金的時間序列有1825條資料

3.2 預測

(1)特征工程

# 提取特征

from tsfresh import extract_features, extract_relevant_features, select_features

from tsfresh.utilities.dataframe_functions import impute

gold_df['id'] = range(len(gold_df))

extracted_features = extract_features(gold_df,column_id='id')

extracted_features.index = gold_df.index

# 去除NAN特征

extracted_features2 = impute(extracted_features)

構造訓練集

import re

# 向未來移動一個時間步長

timestep = 1

Y = list(gold_df['USD'][timestep:])

X_t = extracted_features2[:-timestep]

X = select_features(X_t, np.array(Y), fdr_level=0.5)

X = X.rename(columns = lambda x:re.sub('[^A-Za-z0-9_]+', '', x))

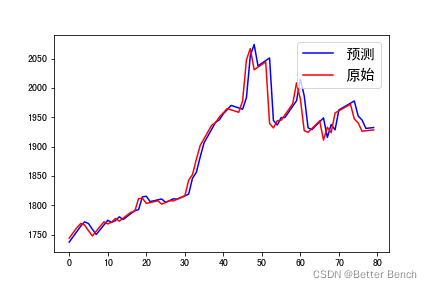

(2)模型訓練預測

# 劃分30%作為測驗集

s = 0.3

tra_len = int((1-s)*len(X))

test_len = len(X)-tra_len

X_train, X_test, y_train, y_test = X[0:tra_len], X[-test_len:], Y[0:tra_len],Y[-test_len:]

# 方法一

import lightgbm as lgb

# clf = lgb.LGBMRegressor(

# learning_rate=0.01,

# max_depth=-1,

# n_estimators=5000,

# boosting_type='gbdt',

# random_state=2022,

# objective='regression',

# )

# clf.fit(X=X_train, y=y_train, eval_metric='MSE', verbose=50)

# y_predict = clf.predict(X_test)

# 方法二

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

import matplotlib.pyplot as plt

linreg = LinearRegression()

model = linreg.fit(X_train, y_train)

y_pred = linreg.predict(X_test)

預測及輸出評價指標

from sklearn import metrics

def metric_regresion(y_true,y_pre):

mse = metrics.mean_squared_error(y_true,y_pre)

mae = metrics.mean_absolute_error(y_true,y_pre)

rmse = np.sqrt(metrics.mean_squared_error(y_true,y_pre)) # RMSE

r2 = metrics.r2_score(y_true,y_pre)

print('MSE:{}'.format(mse))

print('MAE:{}'.format(mae))

print('RMSE:{}'.format(rmse))

print('R2:{}'.format(r2))

metric_regresion(y_test,y_pred)

MSE:267.91294723114646

MAE:10.630377450265746

RMSE:16.368046530699576

R2:0.9707506268528148

可視化預測結果

import matplotlib.pyplot as plt

plt.figure()

plt.plot(range(len(y_pred[100:180])), y_pred[100:180], 'b', label="預測")

plt.plot(range(len(y_test[100:180])), y_test[100:180], 'r', label="原始")

plt.legend(loc="upper right", prop={'size': 15})

plt.show()

3.3 進階的預測方案和代碼

import pandas as pd

import numpy as np

import warnings

warnings.filterwarnings('ignore')

import statsmodels.api as sm

import matplotlib.pyplot as plt

import matplotlib as mpl

import itertools

plt.style.use("fivethirtyeight")

gold = pd.read_csv('LBMA-GOLD.csv')

bitcoin = pd.read_csv('BCHAIN-MKPRU.csv')

gold.index = list(pd.DatetimeIndex(gold.Date))

bitcoin.index = list(pd.DatetimeIndex(bitcoin.Date))

bitcoin['Date'] = bitcoin.index

gold['Date'] = gold.index

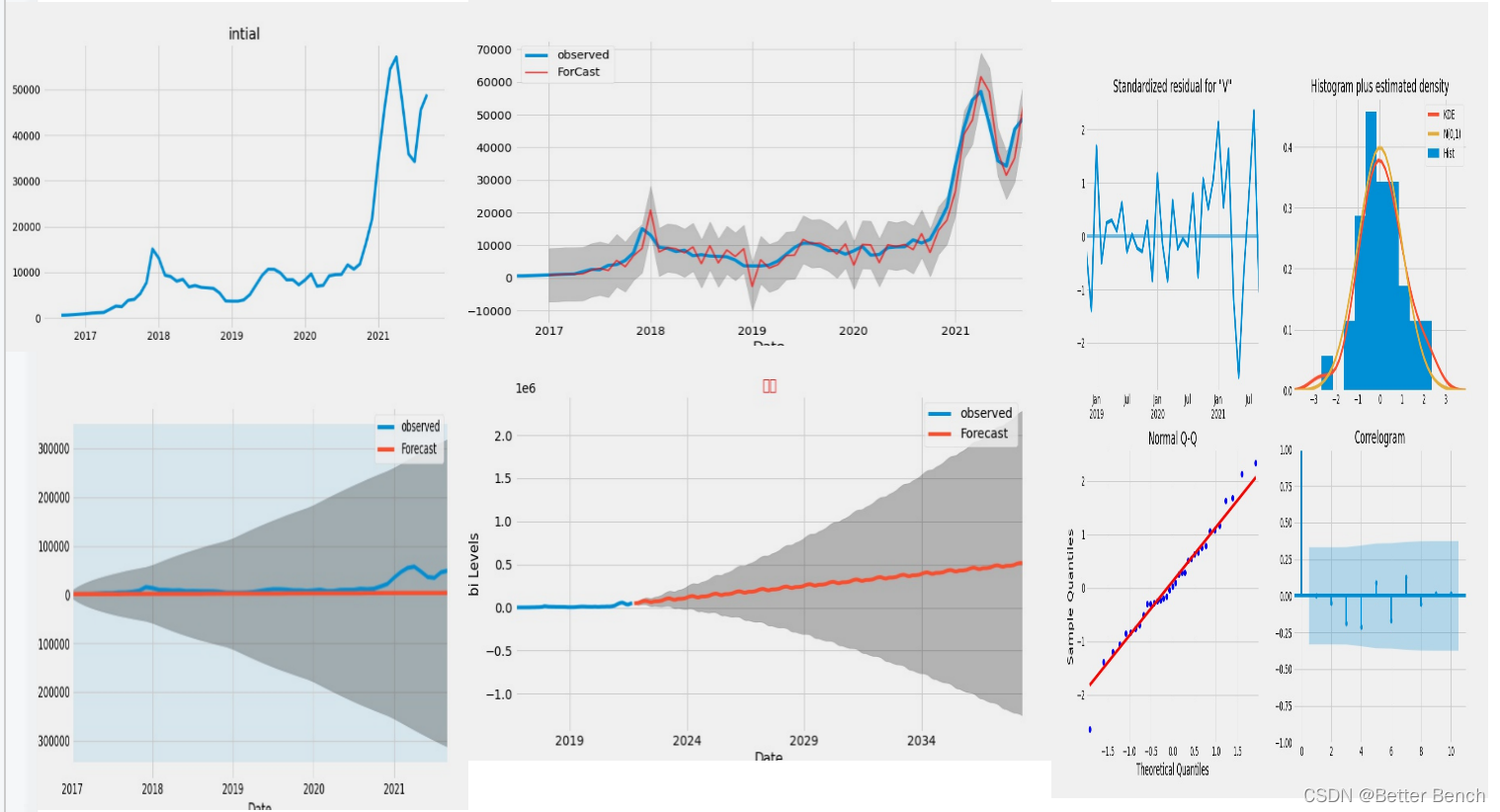

y=bitcoin["Value"].resample("MS").mean()#獲得每個月的平均值

print(y.isnull().sum)#5個 檢測空白值

#處理資料中的缺失項

y=y.fillna(y.bfill())#填充缺失值

plt.figure(figsize=(15,6))

plt.title("intial",loc="center",fontsize=20)

plt.plot(y)

#找合適的p d q

#初始化 p d q

p=d=q=range(0,2)

print("p=",p,"d=",d,"q=",q)

#產生不同的pdq元組,得到 p d q 全排列

pdq=list(itertools.product(p,d,q))

print("pdq:\n",pdq)

seasonal_pdq=[(x[0],x[1],x[2],12) for x in pdq]

print('SQRIMAX:{} x {}'.format(pdq[1],seasonal_pdq[1]))

# 時間序列搜索最優引數(位元幣為例,黃金同理)

for param in pdq:

for param_seasonal in seasonal_pdq:

try:

mod = sm.tsa.statespace.SARIMAX(y,

order=param, seasonal_order=param_seasonal, enforce_stationarity=False, enforce_invertibility=False)

results = mod.fit()

print('ARIMA{}x{}12 - AIC:{}'.format(param, param_seasonal, results.aic))

except:

continue

mod = sm.tsa.statespace.SARIMAX(y,

order=(1, 1, 1),

seasonal_order=(1, 1, 0, 12),

enforce_stationarity=False,

enforce_invertibility=False)

results = mod.fit()

print(results.summary().tables[1])

results.plot_diagnostics(figsize=(15, 12))

plt.show()

# #進行驗證預測

pred=results.get_prediction(start=pd.to_datetime('2017-01-01'),dynamic=False)

pred_ci=pred.conf_int()

print("pred ci:\n",pred_ci)#獲得的是一個預測范圍,置信區間

print("pred:\n",pred)#為一個預測物件

print("pred mean:\n",pred.predicted_mean)#為預測的平均值

#進行繪制預測影像

plt.figure(figsize=(10,6))

ax=y['1990':].plot(label="observed")

pred.predicted_mean.plot(ax=ax,label="static ForCast",alpha=.7,color='red',linewidth=2)

#在某個范圍內進行填充

ax.fill_between(pred_ci.index,

pred_ci.iloc[:, 0],

pred_ci.iloc[:, 1], color='k', alpha=.2)

ax.set_xlabel('Date')

ax.set_ylabel('bi Levels')

plt.legend()

plt.show()

pred_dynamic = results.get_prediction(start=pd.to_datetime('2017-01-01'), dynamic=True, full_results=True)

pred_dynamic_ci = pred_dynamic.conf_int()

# #使用動態預測

pred_dynamic = results.get_prediction(start=pd.to_datetime('2017-01-01'), dynamic=True, full_results=True)

pred_dynamic_ci = pred_dynamic.conf_int()

ax = y['2017':].plot(label='observed', figsize=(20, 15))

pred_dynamic.predicted_mean.plot(label='Dynamic Forecast', ax=ax)

ax.fill_between(pred_dynamic_ci.index,

pred_dynamic_ci.iloc[:, 0],

pred_dynamic_ci.iloc[:, 1], color='k', alpha=.25)

ax.fill_betweenx(ax.get_ylim(), pd.to_datetime('2017-01-01'), y.index[-1],

alpha=.1, zorder=-1)

ax.set_xlabel('Date')

ax.set_ylabel('bi Levels')

plt.legend()

plt.show()

# Get forecast 500 steps ahead in future

pred_uc = results.get_forecast(steps=200)#steps 可以代表(200/12)年左右

# Get confidence intervals of forecasts

pred_ci = pred_uc.conf_int()

plt.title("預測",fontsize=15,color="red")

ax = y.plot(label='observed', figsize=(20, 15))

pred_uc.predicted_mean.plot(ax=ax, label='Forecast')

ax.fill_between(pred_ci.index,

pred_ci.iloc[:, 0],

pred_ci.iloc[:, 1], color='k', alpha=.25)

ax.set_xlabel('Date',fontsize=15)

ax.set_ylabel('bi Levels',fontsize=15)

plt.legend()

plt.show()

完整數學模型和代碼下載

3.4 動態規劃

3.4.1 思路方案

符號說明

w

1

w_1

w1?,

w

2

w_2

w2? 初始買入比例

P

t

P_t

Pt?,

P

t

?

1

P_{t-1}

Pt?1? 前后一天價格

diff 前后一天價格差

Y

t

Y_t

Yt? 變化收益

b% 中途賣出比例(也是買入比例)

目標函式:

m

a

x

max

max

Y

t

Y_t

Yt? =

W

1

W_1

W1?

P

黃

P_黃

P黃?+

W

2

W_2

W2?

P

比

P_比

P比?

約束條件:

1、

C

=

W

1

×

P

×

b

%

×

1

%

+

W

i

×

P

×

b

%

×

2

%

C=W_1×P × b\% ×1\%+W_i × P × b \% × 2 \%

C=W1?×P×b%×1%+Wi?×P×b%×2%(成本約束)(買出賣出成本)

2、

X

i

=

{

0

x

0

=周末

1

x

1

!=周末

X_i= \begin{cases} 0& \text{$x_0$=周末}\\ 1& \text{$x_1$ !=周末} \end{cases}

Xi?={01?x0?=周末x1? !=周末?

3、diff=

P

t

P_t

Pt?-

P

t

?

1

P_{t-1}

Pt?1? (持有會帶來的成本)

4、

0

≤

r

≤

1

0 \leq r \leq 1

0≤r≤1 風險系數約束(可用預測模型的置信區間權衡風險)

3.4.2 思路2

符號說明

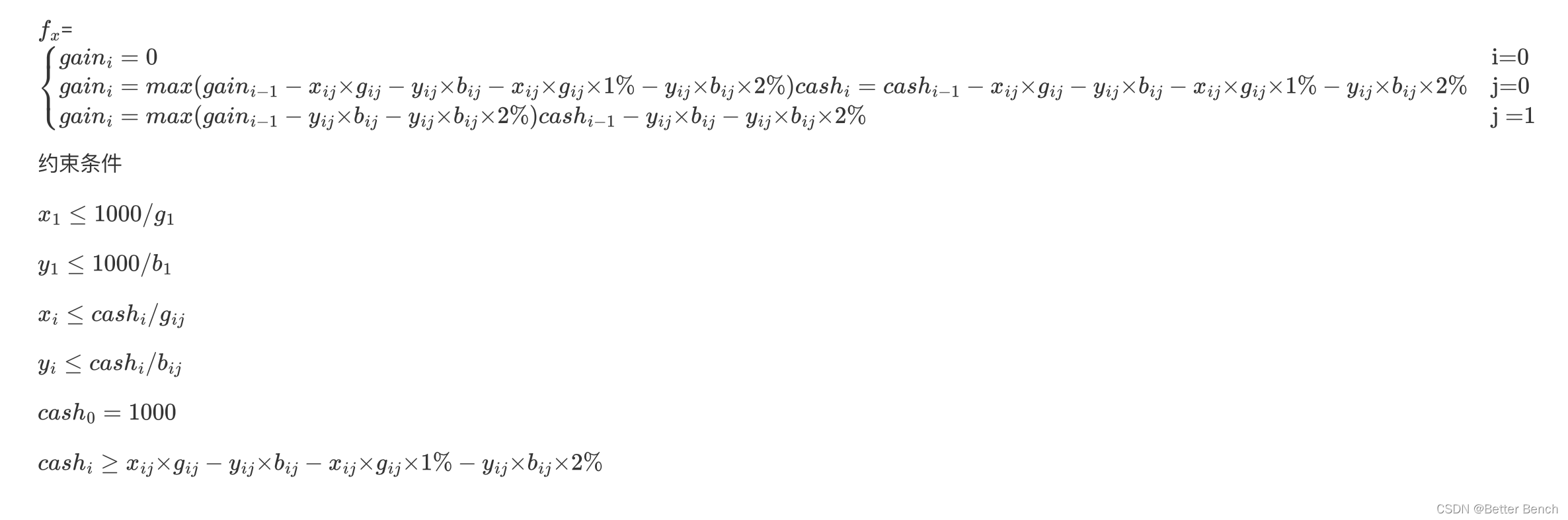

目標函式 M a x ∑ i n g a i n i Max {\sum _i^n{gain_i}} Max∑in?gaini?

i表示第i天的交易,取值1-n

j表示是否是周末,取值0或1,0表示不是周末, 1表示周末

g a i n i gain_i gaini?表示第i天的最大收益

g i j g_{ij} gij?表示第i天的黃金價格

b i j b_{ij} bij?表示第i天的位元幣價格

x i j x_{ij} xij?表示第i天購入的黃金數量,單位美元/盎司

y i j y_{ij} yij?表示第i天購入的位元幣數量,單位美元/個

g_i =[5,20,56,23,4,5,6]

b_i =[2,3,4,4,5,5,66,7]

3.4.3 思路3

我們用buy表示在最大化收益的前提下,如果我們手上擁有一支股票,那么它的最低買入價格是多少,在初始時,buy 的值為prices[0] 加上手續費fee,那么當我們遍歷到第 i (i>0) 天時:

如果當前的股票價格prices[i] 加上手續費fee 小于buy,那么與其使用buy 的價格購買股票,我們不如以prices[i]+fee 的價格購買股票,因此我們將buy 更新為prices[i]+fee;

如果當前的股票價格prices[i] 大于buy,那么我們直接賣出股票并且獲得prices[i]?buy 的收益,但實際上,我們此時賣出股票可能并不是全域最優的(例如下一天股票價格繼續上升),

因此我們可以提供一個反悔操作,看成當前手上擁有一支買入價格為 prices[i] 的股票,將buy 更新為prices[i],這樣一來,如果下一天股票價格繼續上升,

我們會獲得prices[i+1]?prices[i] 的收益,加上這一天prices[i]?buy 的收益,恰好就等于在這一天不進行任何操作,而在下一天賣出股票的收益;

對于其余的情況,prices[i] 落在區間[buy?fee,buy] 內,它的價格沒有低到我們放棄手上的股票去選擇它,也沒有高到我們可以通過賣出獲得收益,因此我們可以賣出去交易位元幣,

上面的貪心思想可以濃縮成一句話,即當我們賣出一支股票時,我們就立即獲得了以相同價格并且免除手續費買入一支股票的權利,在遍歷完整個陣列prices 之后之后,我們就得到了最大的總收益,

3.3.2 Python實作

完整數學模型和代碼下載

轉載請註明出處,本文鏈接:https://www.uj5u.com/qita/429539.html

標籤:其他